Money is like Oxygen

Money, while it is not everything, it is pretty close to oxygen on the list of “gotta have it.”

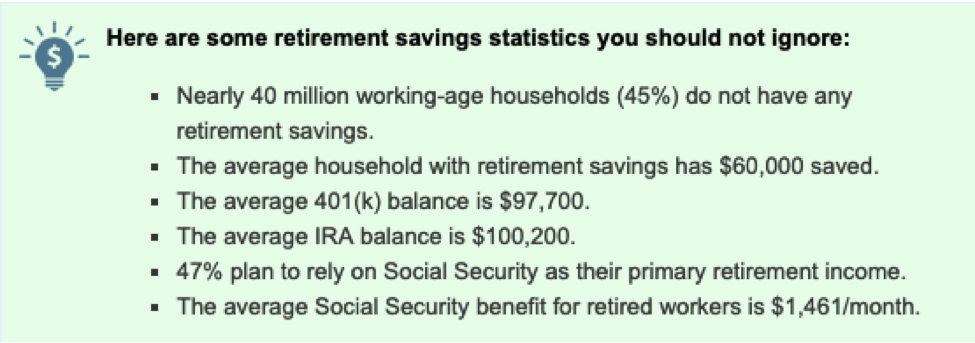

“When it comes to average retirement savings statistics in America, the picture is fairly bleak.”[1]

“The first thing to know is that the average American has nothing saved for retirement, or so little it won’t help. By far the most common retirement account has nothing in it.”[2]

“Most Americans don’t have nearly enough saved for retirement. If you have big plans for retirement, it means sacrificing now. You’ll need to exchange instant rewards for a better later life.”[3]

I have been working with individuals and their money since 2008 and the story of how to gain financial freedom and independence without sacrificing too much lifestyle in the future has not changed – YOU MUST SAVE THE MONEY!

There is no get rich quick scheme.

There is no network-marketing business that will turn you into a millionaire entrepreneur. There is no one investment that will take you over the top and solve all your problems. Even my beloved custom-designed, dividend paying, non-direct recognition whole life insurance assets from a mutual company will not ensure you are able to maintain the lifestyle to which you have been accustomed. The one “asset” that will save you is YOU saving your own as$!

In addressing the bondage women had endured and accepted for centuries, Betty Friedan touched upon a human truth: we are all in bondage to that which we don’t question but rather accept because “this is what everyone else does…this is what is accepted…this is what I have been told.” The problem with following the masses is that the “m” is often silent.

“It is easier to live through someone else than to complete yourself. The freedom to lead and plan your own life is frightening if you have never faced it before. It is frightening when a woman finally realizes that there is no answer to the question ‘who am I’ except the voice inside herself.”

― Betty Friedan

So who do you want to be?

Do you want to be like the uber-majority of people who have so little they MUST downsize in a dramatic fashion and even become fully dependent on family, the community, the government…strangers?!

If your response is, “I don’t have enough money to save for my future,” let’s examine statistically how much you REALLY have. How much does a household (understood to be 4 people) have to earn to be considered “Top X% of Household Income in America” as of 2018:

1%… $434,454.80

5%… $236,360.40

10%… $178,793.00

20%… $127,144.40

30%… $98,823.20

35%… $ 86,599.91(Avg. household income 2018)

40%… $78,567.20

50%… $61,822.00 (Median household income 2017)

60%… $48,002.00

70%… $35,494.60

80%… $24,913.40 (poverty level for family of 4)

90%… $ 14,280.00 ($12,140 is poverty for 1)

According to the “Global Rich List,” a website that brings awareness to worldwide income disparities, an income of $32,400 a year will allow you to make the cut – you are in the world’s 1% for 2019. MedianU.S. wealth of $61,667 – that’s the amount where half of people have more and half have less – far outpaces other parts of the globe.

On a global scale, the vast majority of Americans are either upper-middle income or high income.

Many Americans who are classified as “poor” by the U.S. government would be middle income globally. The bottom 10% of the U.S. income distribution falls in the upper 30% of the global income distribution. Someone at the poverty line in the United States is in the top 14% of the global income distribution. Almost nine-in-ten Americans had a standard of living that was above the global middle-income standard.

If you are like some of us, you might hear the annoying and oh-so-ineffective, “There are people starving in China. Eat your peas,” and, as such, you are not motivated to change. On the other hand, you may have grown up a little and have a mind of a responsible and rational adult and you realize, “Holy smokes, I need to reevaluate how I think about and manage my money as I truly have more than enough.”

If none of those thoughts when through your mind, because you still “feel” like you are “poor,” especially if you are the typical American adult who carries $60,205 in debt,let’s examine how much you need to earn in the US to be considered the “Top X% of Salary Earners:”

1%… $ 250,000

5%… $ 135,000

10%… $ 95,000

20%… $ 65,000

30%… $ 50,000

40%… $ 40,000

50%… $ 30,000

60%… $ 20,000

70%… $ 15,000

80%… $ 5,000

90%… $ 4,999 or less

In the end, NO ONE IS WITHOUT EXCUSE.

People are destroyed for lack of APPLICATION of knowledge. If you want any semblance of a secure financial life, YOU must save the money. YOU must manage your passions and wants so you can set aside 20ish percent so you WILL have a future without dependence on your children, the community, the government, strangers!

I became a financial advisor in 2008 because I was fully aware of how outrageously difficult it is to accept and then FOLLOW “Truth.” MONEY IS NOT MATH. MONEY IS HUMAN BEHAVIOUR. It is my heart’s desire to see people prosper financially in the here and now but, alas, I can not help those who won’t heed advice. If you want more than the false and empty advice the (m)asses follow, let’s talk. Otherwise, please know, I am here when you are ready.

I’m excited to walk this journey with you as we unveil the practical and research-based information on how to achieve that which we all desire for ourselves and others – to be “happy”. We discover that happiness is attainable and, better yet, sustainable, as long as one is willing to do the work. In my book “The Happiness Formula”, I dive into each element in detail. Order your copy of “The Happiness Formula”, click here and subscribe to my YouTube Channel (click here) for continued insights and updates into HAPPINESS. Thank you for your support!

Kasandra Vitacca Mitchell

Kasandra Vitacca Mitchell is an Author, Speaker, Coach of Wealth & Happiness with a mission to bring research, wisdom, and authenticity to others via “The Happiness Formula.”

[1]“Average Retirement Savings: Are you Normal?” SmartAsset.com, April 2019; [2] “Average Retirement Savings 2019,” TheStreet.com, March 2019; [3]“Average Retirement Savings,” CreditDonkey.com, April 2019